The S&P 500 is hovering near all-time highs, but beneath the surface, something has shifted. The "Magnificent Seven"—the tech giants that powered the market’s relentless rise—are showing cracks. AI capital expenditure (CapEx) is slowing, inflation is proving stickier than expected, and the Federal Reserve’s next moves are far from certain. For investors, the question is no longer whether the bull market will continue, but how to hedge against the turbulence ahead.

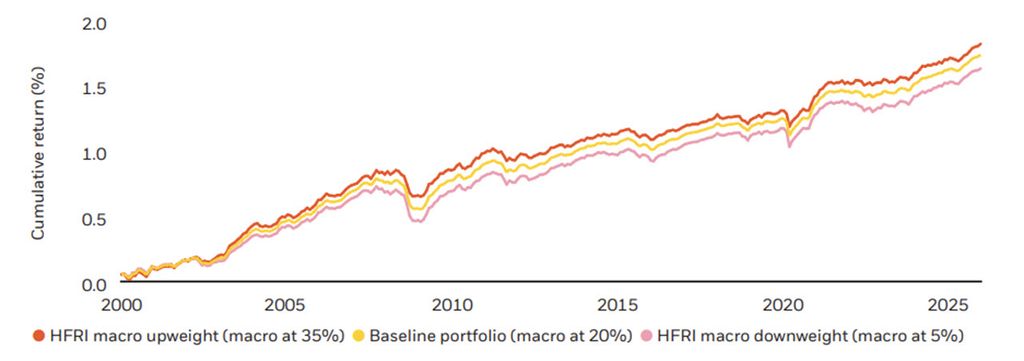

The traditional playbook for portfolio hedging—loading up on bonds, gold, or defensive sectors—is being rewritten. Institutional reports from BNP Paribas, Barclays, and Morgan Stanley suggest that quant multi-strategy, global macro, and market-neutral approaches are now the preferred tools for uncorrelated protection. But why? And what does the evidence actually say about these shifts?

The Inflation Paradox: Why Sticky Prices Change Everything

Darius Dale, founder and CEO of 42 Macro, argues that the market is on the cusp of a critical transition: from pricing in peak inflation to pricing in sticky inflation. This isn’t just semantics. If inflation remains elevated, the Fed’s next move could be far more aggressive than investors anticipate—or far more dovish. The evidence, however, is mixed.

One key driver of sticky inflation is AI CapEx. The $800 billion projected for 2026 represents roughly 2.5% of U.S. nominal GDP—a demand shock so large it’s difficult to quantify. But here’s the catch: while AI CapEx has fueled growth, its productivity payoff remains uncertain. Companies are throttling back on compute usage because the promised efficiency gains haven’t materialized yet. This creates a timing mismatch—spending is high, but productivity lags, putting upward pressure on prices without corresponding economic output.

Then there’s the Fed. Dale suggests that the central bank may need to "regain credibility" on inflation by tightening policy further, even if it risks a market correction. This aligns with historical patterns: in 1998, the S&P 500 rallied 20% before a 20% pullback, only to finish the year up 29%. The lesson? Corrections can be violent, but they’re not always the end of the bull market.

The Hedging Playbook: What Works in 2026?

If bonds are no longer the reliable hedge they once were, where should investors turn? Institutional reports highlight three key strategies:

1. Quant Multi-Strategy: Diversified, rules-based approaches that exploit market inefficiencies without relying on directional bets. 2. Global Macro: Flexible strategies that capitalize on macroeconomic trends, including currency fluctuations and commodity cycles. 3. Market-Neutral: Long/short equity strategies designed to profit from relative value rather than market direction.

These approaches share a common goal: uncorrelated returns. In a world where traditional asset classes are increasingly synchronized, diversification alone isn’t enough. The evidence suggests that market-neutral and global macro strategies, in particular, have outperformed during periods of inflationary pressure and Fed tightening.

But there’s a catch. These strategies require sophistication, access to institutional-grade tools, and a willingness to accept complexity. For most investors, the practical alternative is to rebalance portfolios toward equal-weight indices, mid-caps, and international equities—areas that have been overlooked but stand to benefit from AI diffusion and valuation compression.

The Delinquency Dilemma: A Recession Signal or a False Alarm?

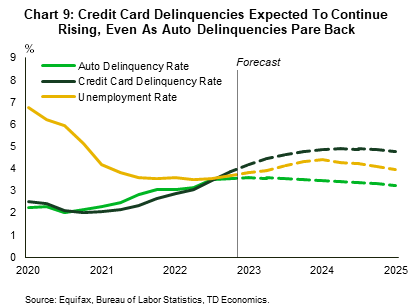

Dale points to rising delinquency rates in credit cards, auto loans, and student loans as evidence of a "recession at the bottom of the economy." On the surface, this seems alarming. Aggregate delinquency rates are near levels last seen during the Great Recession. But the story is more nuanced.

First, delinquency rates are not uniformly distributed. Lower-income households and subprime borrowers are driving the increase, while higher-income groups remain resilient. Second, the relationship between delinquencies and recessions is not linear. Post-2008, regulatory changes and lender behavior shifted, making delinquencies a lagging rather than leading indicator. Finally, the Fed’s response matters: if policymakers view delinquencies as a structural issue rather than a cyclical one, they may hesitate to cut rates, prolonging the pain for borrowers.

The Fed’s Task Forces: A Dovish Pivot or Wishful Thinking?

Dale’s most provocative claim is that the Fed’s five task forces—focused on inflation, productivity, communications, balance sheet, and data—will ultimately lead to a "much more dovish monetary policy" in 2027. The logic? The Fed needs to regain credibility on inflation before it can ease, but once it does, the floodgates will open.

This is speculative. While the task forces are real, their outcomes are far from certain. The Inflation Task Force, for example, could recommend tighter policy if inflation remains stubborn. The Productivity and Jobs Task Force might conclude that AI-driven productivity gains are overstated, justifying higher rates for longer. The evidence here is thin, and the Fed’s internal debates are opaque.

What is supported by evidence is the idea that the Fed’s reaction function is evolving. Quantitative tightening (QT) and reserve management purchases are tools the Fed has used sparingly, but they could become critical in 2026. If the Fed signals a willingness to accelerate QT, bond markets could react violently—creating both risk and opportunity for hedged portfolios.

Where the Puck Is Going: The Case for Broadening Exposure

Dale’s core thesis is that the "puck has left" the Magnificent Seven. The evidence supports this, but with caveats. AI diffusion is real, but its pace and impact are uncertain. Valuation compression between the Magnificent Seven and the rest of the market is underway, but it’s not a linear process. International equities and mid-caps are undervalued, but they come with their own risks (e.g., geopolitical instability, currency fluctuations).

For investors, the takeaway is clear: hedging in 2026 requires more than diversification—it requires adaptability. The strategies that worked in the past (bonds, gold, defensive sectors) may not work in a world of sticky inflation, AI-driven volatility, and evolving Fed policy. The smart money is rotating toward uncorrelated strategies, equal-weight exposures, and global macro bets. The question is whether you’re ready to follow.