The S&P 500 is at record highs, but beneath the surface, economists warn of a looming recession by 2026. The culprit? A perfect storm of AI-driven inflation, Fed policy missteps, and a bottom-heavy economy already showing cracks. Darius Dale of 42 Macro argues the market’s current trajectory is unsustainable—and investors need to prepare now.

The Recession Signals You’re Missing

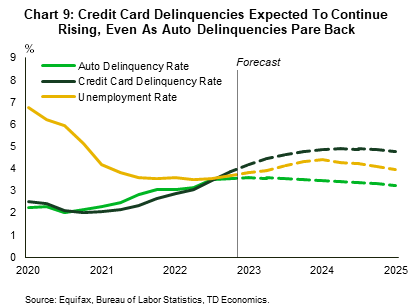

Dale’s warning starts with a sobering fact: the bottom of the U.S. economy is already in recession. Consumer durable goods, residential investment, and nonresidential structures are all contracting. Delinquency rates for credit cards, auto loans, and student loans are at levels last seen during the Great Recession. These aren’t abstract numbers—they’re flashing red lights for the most vulnerable sectors.

AI CapEx: The $1 Trillion Demand Shock

While the bottom struggles, the top is booming—thanks to AI. Hyperscale CapEx (data centers, semiconductors, infrastructure) is projected to hit $1.2 trillion by 2027, a demand shock equivalent to 3.6% of U.S. GDP. This spending is distorting prices for chips, electricity, and labor, creating inflationary pressures the Fed didn’t anticipate.

The problem? Productivity gains from AI won’t appear overnight. Companies are spending billions on compute power that isn’t yet translating into efficiency. If CapEx slows, the ripple effects could trigger a market correction.

The Fed’s Dilemma: Too Little, Too Late?

The Fed is stuck. Inflation is sticky, but rate hikes could worsen the recession in rate-sensitive sectors. Dale’s solution: use the balance sheet (end reserve purchases, restart QT) to signal credibility on inflation. If the bond market doubts the Fed, long-term rates could spike, tightening financial conditions abruptly.

Where’s the Smart Money Going?

Dale’s contrarian take: The Mag 7 are no longer the best place to be. Their free cash flow is being consumed by AI CapEx, and valuations are stretched. Instead, he recommends rotating into mid-caps, small-caps, and international equities—segments poised to benefit from AI-driven productivity gains.

This isn’t just a hunch. When China joined the WTO, its markets outperformed U.S. equities by 500 percentage points over a decade. AI could have a similar diffusion effect, spreading productivity gains across sectors and borders.

Investor Playbook: How to Prepare

Dale’s strategy for navigating the next phase:

The Biggest Risk: Sticky Inflation

The market is pricing in peak inflation, but Dale warns the bigger risk is sticky inflation—price pressures that refuse to fall to the Fed’s 2% target. If he’s right, the Fed may have no choice but to tighten policy, even if it risks a recession. The bond market’s reaction will determine whether 2027 brings a dovish pivot or a hard landing.

The bull market isn’t dead, but the easy gains may be. The next phase will require discipline, patience, and a willingness to look beyond the usual suspects. As Dale puts it: Skate to where the puck is going.